Eurozone Bond Trading Part 2: Shadow Banking (Carry)

Who needs a license?

Intro

In my last article above, I demonstrated that when a country joins the Eurozone, the spread in its bond yields tends to decrease relative to other Eurozone countries. The issue with such trade (Merger Arbitrage), is if there isn’t many countries joining the Euro (akin to not much M&A activity), then there isn’t much to do and PnL to bring in. Thus, is there a complementary trade out there we can deploy, to bring in consistent profits? Yes. Introducing the Shadow Banking Trade (Carry).

Shadow Banking Explained

What does a bank do? Let me give you the classic 3-6-3 example:

3 - Offer 3% interest on deposits

6 - Lend those deposits at 6%, thus capturing 3% spread

3 - Be on the golf course by 3pm (I prefer football, but you get the idea)

Now the reason I use the word shadow here, is because we’ll be doing this though without a banking license. Similar to Le Chiffre in Casino Royale who didn’t have one either, we’re going to borrow money from one source and then lend it to another (albeit he used deposits to short sell airlines stocks and play poker, we’re going to do something a bit less risky).

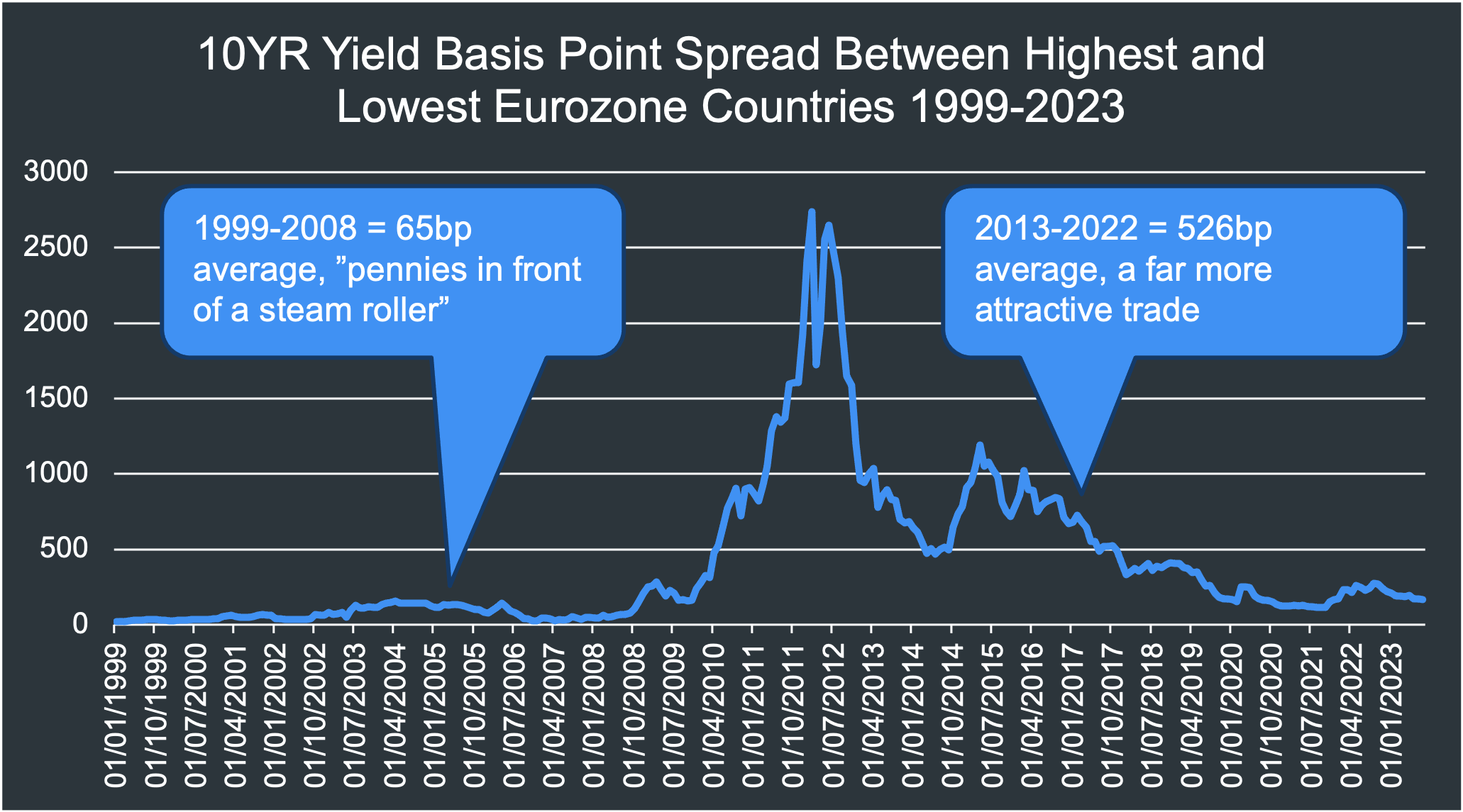

There’s 20 countries in the Eurozone, with credit ratings today varying from AAA (Germany) to BB+ (Greece). So unsurprisingly there is a fair spread between the 10 year bond yields within the Eurozone, although it hasn’t always been this way. See chart below:

The beauty of this trade, is you’re not exposed to FX risk unlike many similar Carry trades, because every country is using the same currency (Euro). So it’s safer, right? Let’s find out.

Methodology

We’re using the same data from the previous article which is from the OECD (main source) and ECB (x3 which OECD didn’t have). Very simple:

Borrow/go short the country which has the lowest yield (aka offer 3% on deposits)

Lend/go long the country which had the highest yield (aka lend to another at 6%)

Close the trade every January, and then re-deploy it to the new highest/lowest yielding country. In practice this means borrowing from Germany all the time, then lending to Greece most of the time (apart from 1999 = Italy, 2000 = Portugal, 2005 = Italy)

Profit Explained (see note 1):

If the spread in Jan is 200bps/2% (e.g. Germany at 3% and Greece at 5% yields), and the following January it’s still a 200bps/2% spread, then our profit is 200bps (Carry)

However if the spread widens 50bps, then we only collect 150bps (200 - 50). This is because the bond we have bought has dropped in value, relative to the bond we have shorted. The opposite is true if the spread tightens - the bond we have bought increases in value, and we gain extra profit.

Note 1: In reality you’ll never get this exact PnL due to bond duration and the shape of each countries yield curve, although using futures and other derivatives can help get the desired exposure. That said, whether this backtest is fully accurate or simple, the message and findings from the article would still be the same.

Results

When it worked

Over 23 years it had 5 negative ones, so profitable 8/10 years. I’ll take that. Thus a great complementary strategy to our Macro Merger Arb in Part 1, which doesn’t always have a trade on. As you can’t just sit in cash for ages, otherwise investors ask what they’re paying a management fee for. However you may have noticed the tombstone emoji in 2012, representing a wipeout as Greece went onto default/restructure its debt (see note 2).

Note 2: It is challenging to estimate losses in 2012 as it depends on what you bought the bond for, however based on the Bank of Greece’s data, you’d have bought the bond at €34 per €100 in Jan 2012 and 5 months later it dropped to €17 resulting in a 50% drop. Let’s face it, you’d have been wiped out, hence me not attempting to calculate PnL for 2012.

When it didn’t work

Where you given a heads up as to the default? From 2009, the trade started to go against you when the Eurozone Debt Crisis began which was certainly sped up by the prior Financial Crisis, that hit our Slovakian Merger Trade in the previous article.

From here one event led to another, and as shown above you’d have lost 11 years of profit in 1 year and been wiped out, even before the default. Would you have continued? Inevitably, you’d be fired and/or face massive investor redemptions, because most people exhibit recency bias.

However, for those who had listened to Nathan Rothschild’s “Buy when there is blood in the streets” advice which has served investors pretty well over the centuries, here’s what you would have made “carrying” on after the debt restructure.

As shown, you’d have made a fortune thanks to Mario Draghi using the full firepower of the ECB, to bring yield spreads back under control (essentially pushing up the price of Greek Bonds relative to Germany’s). As well as the massively elevated spread/carry, because who wants to lend to someone that just defaulted? Could you have known this would happen? Even one the world’s best, Michael Platt at the time said you could make a “pretty sensible argument for almost any outcome in Europe.”

Recommendations to Investors

1. Understand the skew of your strategy

Had you started doing this trade in 2011, you’d have lost money ➡️ probably thought it was a bad strategy ➡️ stopped doing it. Though as demonstrated above, it’s profitable 8/10 years and can make quite good PnL. So if you take time to understand the skew your strategy faces, you’ll likely become more comfortable taking loses, knowing this is part of normal business.

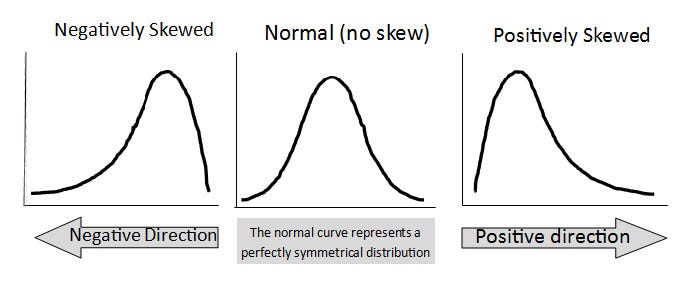

Let me explain skews using these charts below:

Normal Skew = You win about 50% of trades. Some big winners, some big losers.

Positive Skew = You lose on the majority of trades, though win big on some

This is what Equities and Commodities typically exhibit

Negative Skew = You win on the majority of trades, though sometimes suffer big losses.

This is what Bonds and FX carry strategies typically exhibit (which this trade belongs too)

If you’re still completely lost, imagine you’re playing on a slot machine. You won’t win most spins, then now and again you’ll win lots. You therefore face a positive skew. Whereas the Casino will collect money on most spins, then occasionally lose a lot. They therefore face a negative skew.

Conclusion

Does it make consistent profits? Yes. Can it blow up? Yes. So we need to find a final strategy to protect us during events like this, which we’ll explore in Part 3. Stayed tuned.

Hope you learnt something new

Chris