How to be a Champions League Investment Manager

Buy low, sell high right?

Intro

There are 1,070 professional football clubs in Europe, yet only 32 (3%) make it into the Champions League. It’s similar stats in fund management, in that most active managers do not beat passives (see page 17). However there’s some that do, and really are Champions League Fund Managers. Let me give you an example - Millennium.

For those not familiar, the S&P 500 has a long run Sharpe of around 0.4 (see note 1 regarding comparison to S&P 500). So objectively speaking, here’s a fund that:

Has multiple times better risk adjusted returns than passives, and many other fund managers (like scoring far more goals than they are conceding)

Has never had a major drawdown like many passives and other fund managers (like never falling into a relegation battle)

Now the real question is, how do we get to that level?

Well Market Wizards and Inside the House of Money books, are a great place to start for interviews with some elite managers. Though interviews like these tend to be long stories, short evidence. So how can we flip this round, to actually figure out what’s driving fund manager returns? Well, AQR have done just that over several academic articles titled the “Superstar Investors” series. Quantifying the returns of several star managers (Buffet, Soros etc) into Alpha, Beta and Factors (e.g. Value, Momentum) respectively.

So thought I’d combine data from all articles into one, and try to draw insights into how to make it into the Champions League.

Note 1: Appreciate this isn’t Millennium’s benchmark, though would need 10+ benchmarks to accurately assess a multi manager platform. Thus going with the generic one, which is still quite useful.

Methodology

Take all AQR Superstar Investor articles (believe there’s x4, please correct me if I’m wrong. I dropped x1 “Spain’s Value Investors” as the time horizons in this paper were too short to draw conclusions).

Create a table, combining data from all of them.

Cross reference with other information, draw some conclusions.

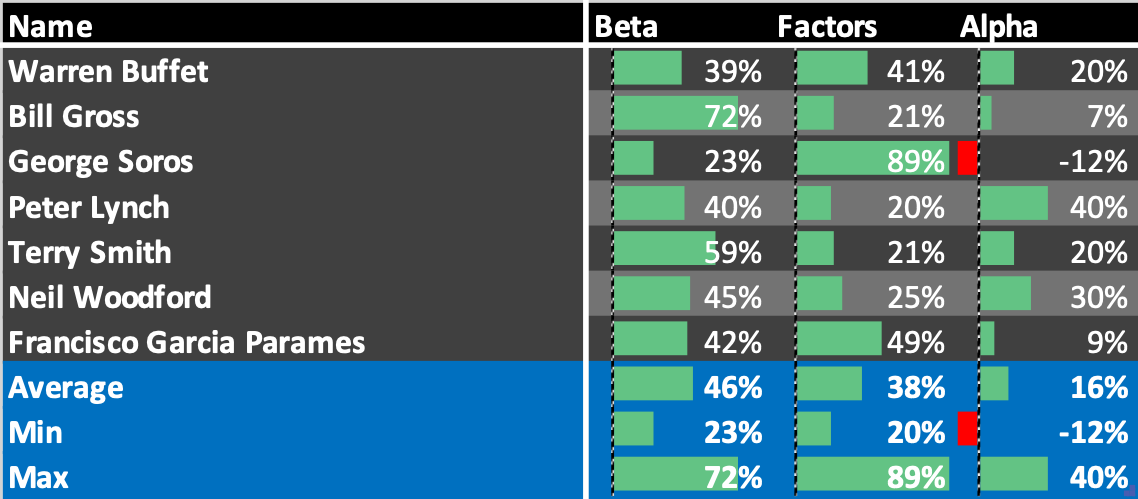

The Results

Below is a table I’ve made, showing what percentage of each fund manager’s returns are due to the 3 elements mentioned above. See Note 2 regarding Soros’s Beta and Note 3 regarding Negative Alpha. I’ll then draw some conclusions below:

Note 2: Soros was likely Absolute Return given he’s Global Macro, rather than having a specific benchmark. I therefore treat the long Equity return component as Beta.

Note 3: Based on Note 2 and the fact that Soros basically traded everything, it’s no surprise that the regressions done in the paper, came to a funny negative Alpha result. No model is perfect, though this research certainly gives a better insight into fund manager performance than otherwise would be the case.

Insight 1: Get long and stay long

The Beta column is fascinating. On average, almost half of these elite manager returns are beta. What this means is, they just got long and stayed long a decent amount of their benchmark. Sounds really easy right? Though imagine being Bill Gross running over $250bn in bonds (admittedly this has grown over time, though you get the idea) and living through:

1994 Bond Market Rout (hit Steinhardt)

1998 Russia Default (hit LTCM)

2000 Tech Bubble (hit Tiger, though long live the cubs)

2008 Housing Crash (hit Lehman Brothers)

In all these events, default rates will have spiked and bond yields moved violently. Thus surviving through such times and staying long, is a lot harder than it sounds. As demonstrated by the great managers and institutions mentioned above, getting hit badly during such times.

Insight 2: Factors help

Add Factors to the Beta, and you realise another 40% or so of these returns, can be explained by well known factors. Thus in a simple equation based on averages:

46% Beta + 38% Factors + 16% Alpha = Superstar Manager

Notice how Alpha is the smallest component? So again whilst it is tempting to re-invent the wheel, by making some funky quant models or coming up with a unique approach. You can evidently rise to the top, just by utilising what is already known and well documented. For example, the Intelligent Investor which advocates the Value Factor was released in 1949, some 70+ years ago.

I just want to clarify that many of the above managers are unlikely to call themselves Factor investors, though their returns can certainly be explained by them.

Recommendations to Investors

I’m going to make 2 practical recommendations - one for those running money (e.g. fund managers, retail investors) and one for fund manager selectors (e.g. multi manager strategies like Millennium, pension funds etc).

Those running money: Find factors you believe in

What’s evident is that the best fund managers find Factors they believe in (consciously or unconsciously), and stick with them. Ideally use multiple factors at once (e.g Value and Momentum being great as they’re negatively correlated), though even just one should help you deliver a bit more than Beta (the market) over the long term.

For example, Buffet’s Factors in simple terms include:

Quality - The firm’s with big moat’s/a sustained competitive advantage

Low Risk - Low Beta stuff

Value - Low price to book

Fund Allocators: Pay attention to Beta

Breaking down a Fund Manager/Traders returns into Factors maybe difficult without the right software, though Beta should be relatively straightforward as it’s on most Morningstar factsheets. Let me explain why Beta matters beyond risk and returns:

Say you have an active fund costing 1% with a Beta of 0.9

S&P 500 Tracker cost = 0.07%

Cost difference = 0.93%, meaning if the fund manager beats the index by 1% consistently (which most managers would be content with) you’ll basically see none of that extra return after costs.

This sounds super obvious, though I’ve never heard anyone say it out loud (maybe there’s a masquerade in the industry, clearly didn’t get the memo). And you may think this is hypothetical and not empirical, though having just looked on AJ Bell at U.S Equities Funds, I can confirm there’s many funds costing around 1% with Beta’s upwards of 0.8…

I personally see no issue in paying 2 and 20 for those delivering Alpha. What I do object to is:

Paying Prada prices for Primark (try saying it quickly)Conclusion

Appreciate I’ve covered a lot here, so to sum up:

Elite fund manager returns are not rocket science or a dark art, they can be fairly well explained by: Beta + Factors + Alpha = Returns

Have a read around, and find some Factors you believe in. As for generating Alpha, get me a whiteboard and some Moroccan Tea poured like this, and I can give you an answer

Don’t pay high fees for Beta (not that I’m trying to reduce revenues for my own industry)

Hope you found this useful

Chris